Bending Spoons: Europe’s Software Roll-Up Goes Public

Views: 182

Bending Spoons (NASDAQ: BSP), an Italy-based technology holding company, filed its F-1 registration statement with the U.S. Securities and Exchange Commission on Jun 8, 2026, targeting a listing on the Nasdaq Global Select Market. The company is seeking to raise $1.5B in primary capital at a target equity valuation of approximately $20B, with roughly 20% of the post-IPO share capital placed into the public float. The capital structure following the offering will comprise ordinary shares (one vote per share) held by public investors and Class A shares (five votes per share) held exclusively by the four co-founders, a dual-class structure that concentrates governance authority within the founding team. To optimize the share count ahead of the listing, the company executed a 10-for-1 stock split in Apr’26, followed by a 1-for-2 reverse split in May’26. Proceeds will be directed toward general corporate purposes and future acquisitions, with no dividend payments planned in the foreseeable future.

The offering is led by Goldman Sachs International, J.P. Morgan, and Allen & Company LLC as Global Leads, with Wells Fargo Securities, BofA Securities, Jefferies, and Evercore ISI as additional Joint Bookrunners, and a European co-manager syndicate including BNP Paribas, UniCredit, and Intesa Sanpaolo.

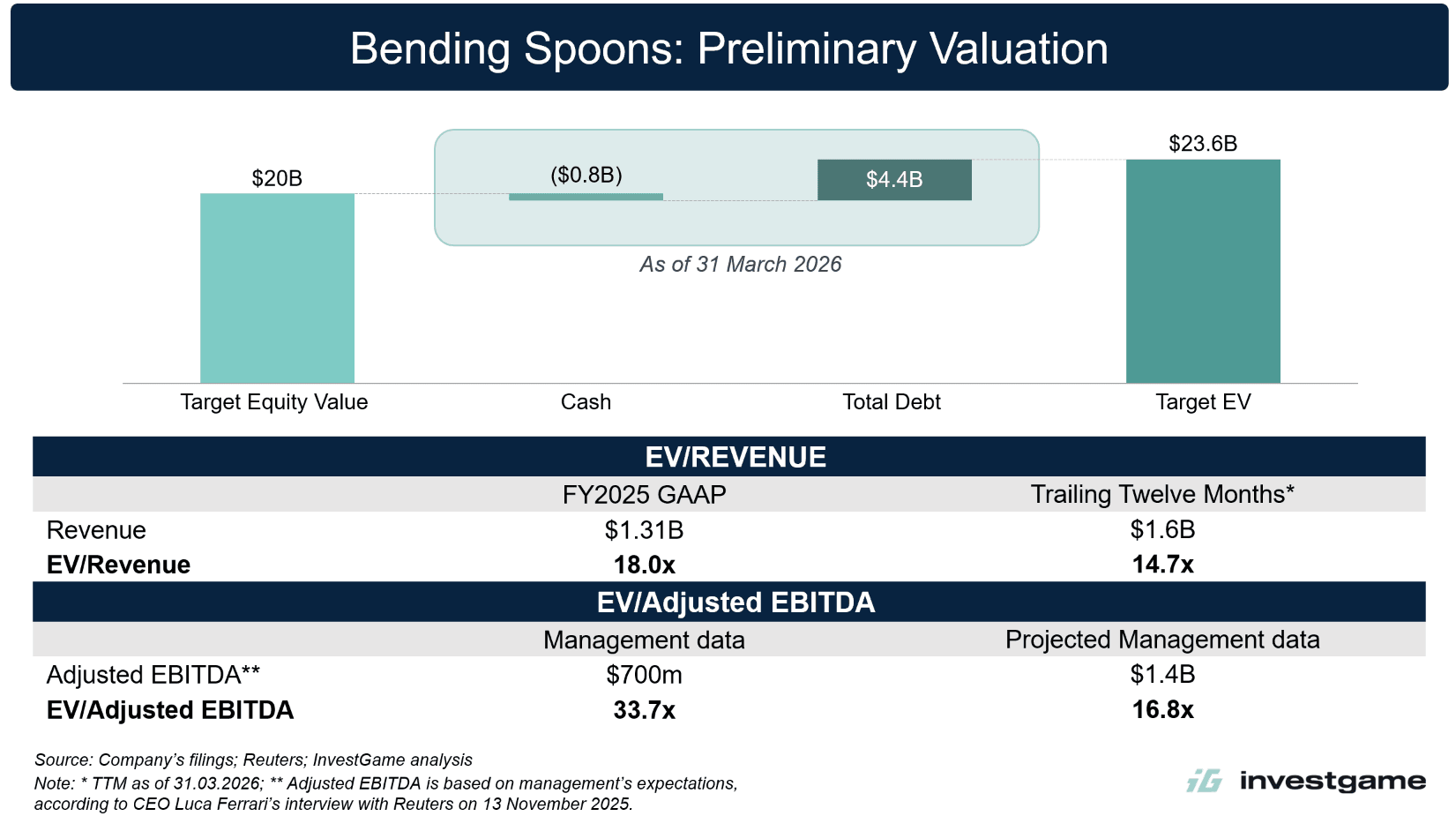

Bending Spoons enters the public market with a $20B target market cap, approximately $3.57B in net debt, and an implied enterprise value of ~$23.57B. The offering prices at 18.0x FY2025 GAAP revenue and 14.7x the trailing twelve-month base of $1.6B revenue through Mar’26. The more consequential question, however, sits on the EBITDA line. At 33.7x on FY2025 adj. EBITDA of $700m, the valuation is built around a forward projection: management guides adj. EBITDA to double to $1.4B in FY2026, for a forward multiple of 16.8x. That step-change is premised on cost synergies from Vimeo, AOL, and Eventbrite, ~$3.38B deployed across three transactions between Nov’25 and Mar’26.

Founded in 2013 by Luca Ferrari, Matteo Danieli, Luca Querella, Tomasz Greber, and Francesco Patarnello, Bending Spoons has grown into one of Europe’s most active digital businesses consolidators, having completed over 50 acquisitions to date. The company’s model is built around a three-step compounding cycle:

- Acquire: The company targets established digital platforms with self-serve subscription or advertising monetization, prioritizing assets with predictable revenue streams within a $50m to $5B annual revenue band, while accounting for potential AI-driven disruption to the target’s business model.

- Transform and Optimize: Following the acquisition, the organization is simplified through significant headcount reductions, codebase overhauls, and subscription price increases, with the goal to shift the asset toward a lean, high-margin operating profile.

- Reinvest: Cash flows generated from the optimized portfolio, combined with debt facilities, fund the next acquisition cycle, continuing the compounding loop.

Between 2023 and Q1’26, the company applied strict internal rate-of-return thresholds to every deal, requiring a 65% hurdle rate on a levered basis and a 25% hurdle rate on an unlevered basis.

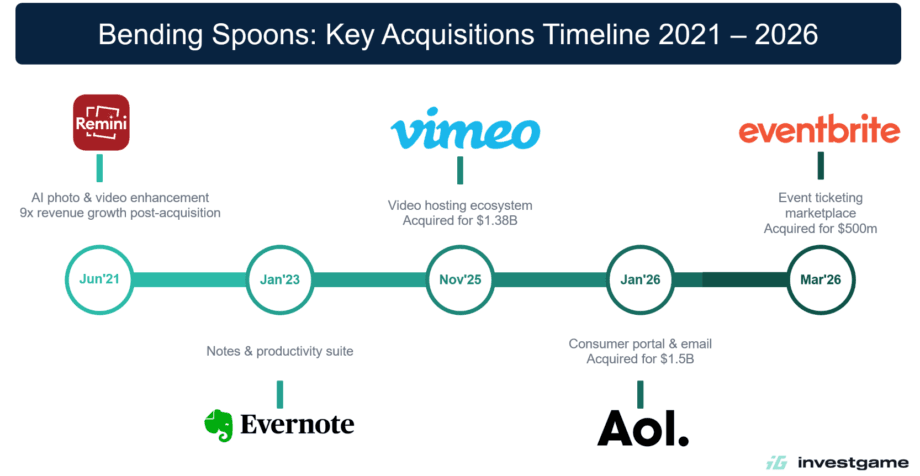

Bending Spoons’ acquisition history has a gaming chapter. In late 2019, the company launched Playond, a mobile gaming subscription service built around a catalog of approximately 60 premium indie titles, which was shut down in early 2020 following consumer backlash from players who had previously purchased those games individually. Since then, the company has directed its strategy exclusively toward subscription digital businesses, creator tools, and legacy internet utilities, with Remini and Evernote establishing the playbook in its earlier phase before capital deployment accelerated sharply into larger, more complex assets at the turn of 2026. Bending Spoons occupies a rare position in the technology landscape: a European-founded operator running a PE-style buy-and-optimize model at a scale more commonly associated with American software consolidators.

The three newest and largest additions, Vimeo, AOL, and Eventbrite, now drive the majority of consolidated revenue. Assets that accounted for 100% of revenue in Q1’24 contributed only 24% of revenue by Q1’26, reflecting the pace of capital deployment. Across the portfolio, subscription revenue retention held at 95% in FY2025 and 94% in Q1’26, supported by a revenue-weighted average subscriber tenure of 8.0 years. Subscriptions account for over 80% of total revenue, with North America generating 65% of Q1’26 revenue and no single customer exceeding 1% of the total. At the operational level, the portfolio has scaled from 111 million MAUs in Dec’23 to 500 million MAUs in Mar’26, with monthly paying customers growing from 3 million to 9 million over the same period.

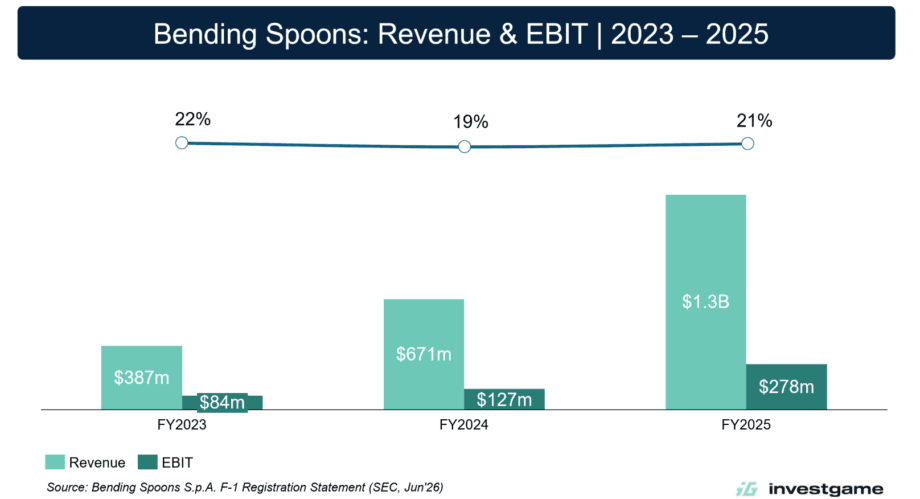

Top-line revenue grew at an 84% CAGR from FY2023 through FY2025, predominantly from adding new assets to the portfolio each year, while existing businesses contributed through new customer acquisition, illustrated by Remini’s approximately 9x revenue growth since its Jun’21 acquisition. Portfolio-wide net revenue retention ranged from 91% to 95% across the period, indicating broadly stable rather than expanding existing subscriber cohorts. The margin trajectory is the more telling signal: despite absorbing successive acquisitions, each carrying its own restructuring costs and overhead burden, EBIT margins held within that 19–22% corridor every year. The intangible asset base supports the same conclusion: the goodwill balance reached $2.42B by Dec 31, 2025, a direct reflection of the pace of acquisitions, while impairment charges totaled approximately $2.4m across the three-year period, relating to a single unit disposed of in FY2025. A clean impairment record alongside stable margins points to acquired businesses holding their value after closing.

We will continue to monitor Bending Spoons’ pricing and early trading performance following its Nasdaq debut, as well as the company’s progress toward its $1.4B FY2026 adj. EBITDA target, and whether its operational compression playbook proves scalable on assets as large and structurally complex as Vimeo, AOL, and Eventbrite.