Feature sponsored by $GDEV

A few years back, the gaming world was buzzing with high-profile exits that grabbed headlines and reshaped the industry’s competitive landscape. Record-breaking IPOs — like Roblox (NYSE: RBLX) and AppLovin (NASDAQ: APP) — hit sky-high valuations. At the same time, giants like Microsoft (NASDAQ: MSFT) and Take-Two Interactive (NASDAQ: TTWO) led the charge in M&A with multi-billion-dollar deals. Video game developers and publishers were at the heart of all this activity, drawing plenty of attention from investors and acquirers.

Over the past decade (2014–2024), the industry saw 42 major exits, each with valuations exceeding $500m. These weren’t just deals; they were proof that investors and founders in the gaming space can achieve meaningful returns in so-called “hit-driven” businesses.

In this article, we’ll dive deeper into these exits and explore:

- The largest public listings and M&A deals in gaming over the past decade

- Which types of exits dominate the industry, and how acquisitions compare to public listings

- The timing of exits, including the average timeline and the most active periods for major deals

- Differences by platform, looking at mobile-first companies vs. those focused on PC and console

For a detailed analysis, check out the accompanying report.

GDEV x InvestGame – Feature #7

Methodology

The entire table with all 42 deals is available exclusively on our Patreon page. Not only does it make your research even more valuable, but it also supports the InvestGame team, enabling us to share even more insights with you. Support us and gain access through the link!

Over the past decade, the gaming industry has seen a wave of high-profile exits, showing how attractive it can be to financial investors and founders. Overall, 42 first-time exits happened via M&A with an upfront enterprise value (EV) above $500m or through public listings with an initial market capitalization of over $500m. For this analysis, we’ve excluded companies that went public or were sold before 2014 – to focus on the first-time exits and uncover how they’ve shaped the industry’s different exit paths.

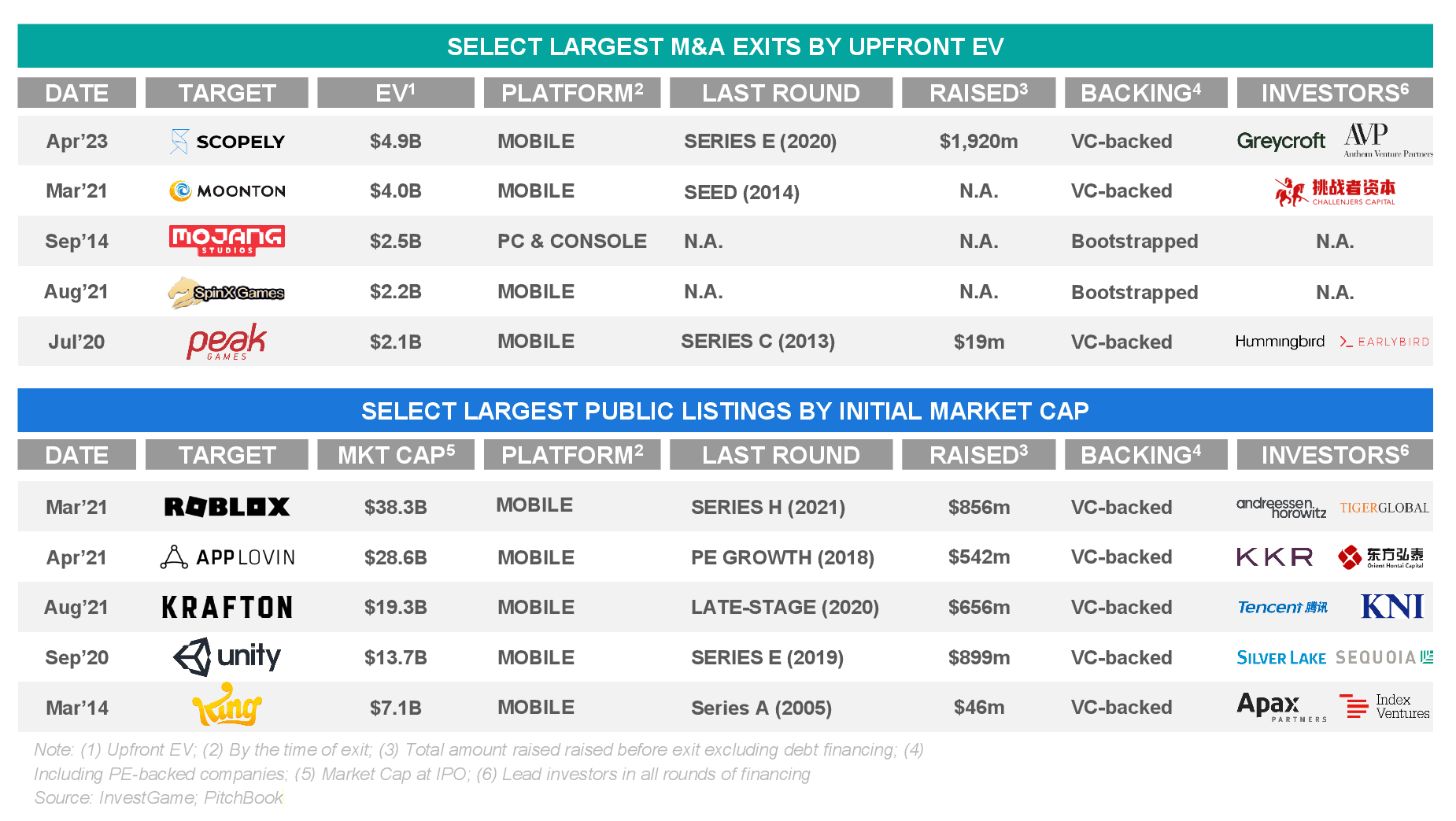

Top-5 gaming M&A and Public listing exits are primarily led by mobile-focused, VC-backed companies

Mobile gaming has genuinely taken center stage, with all top five public listings coming from mobile-first companies (i.e., most of their revenue comes from mobile platforms). Roblox (NYSE: RBLX) leads the pack with a $38.3B market cap at its Mar’21 IPO, followed shortly after a late-stage Series H round earlier that year. AppLovin (NASDAQ: APP) $28.6B and Unity (NYSE: U) $13.7B IPOs underscore the growing demand for gaming ecosystem providers, while Krafton (KRX: 259960) $19.3B IPO in Aug’21 demonstrates how a PC & Console studio can evolve into a mobile-focused business (Krafton’s revenue at listing was mainly driven by mobile titles).

Mobile-focused companies dominate again in the realm of major M&A exits, with Scopely’s $4.9B acquisition in Apr’23 being the largest of its kind. Notably, Mojang Studios stands out as the only PC & Console – focused exit among the top five, acquired by Microsoft (NASDAQ: MSFT) in 2014 for $2.5B – much like Krafton, Mojang eventually made its way onto mobile platforms as well.

VC-backed companies have taken the lead across both M&A (3 out of 5) and public listings (5 out of 5). Success stories like Scopely, Peak Games, Roblox (NYSE: RBLX), and King illustrate how venture capital can help studios scale and reach billion-dollar valuations. Meanwhile, Mojang Studios and SpinX Games are notable examples of bootstrapped achievements, proving that external funding isn’t always necessary when finding the right product-market fit.

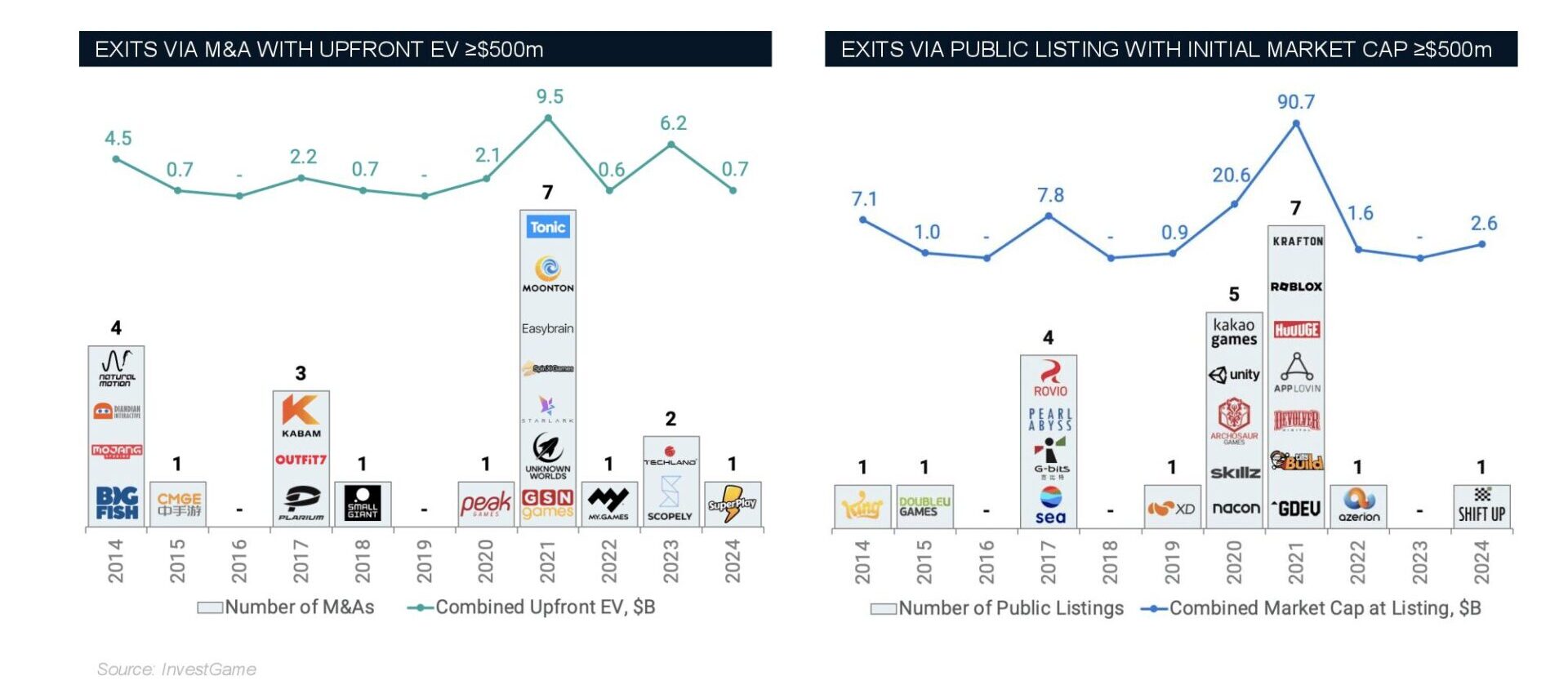

2021 emerged as the busiest year for gaming exits in the past decade, with 14 major deals evenly split between M&As and IPOs

Looking at gaming exits over time, the biggest spikes for both M&A and public listings surfaced during this pandemic-driven period. That year alone saw seven major M&As with a combined upfront enterprise value of $9.5B and seven public listings hitting a total market cap of $90.7B at the time of listing. Supported by a low-interest-rate environment, heightened engagement, and user growth, acquirers and public investors doubled down on gaming. Other periods stayed relatively quiet, except for 2017, which recorded an evident rise in exits.

On a median, about two “successful” (above $500m) exits yearly – one via M&A and one through an IPO. Even though the market has cooled more recently, with higher interest rates and greater caution from investors and acquirers, we still see a steady flow of exits among game developers and publishers.

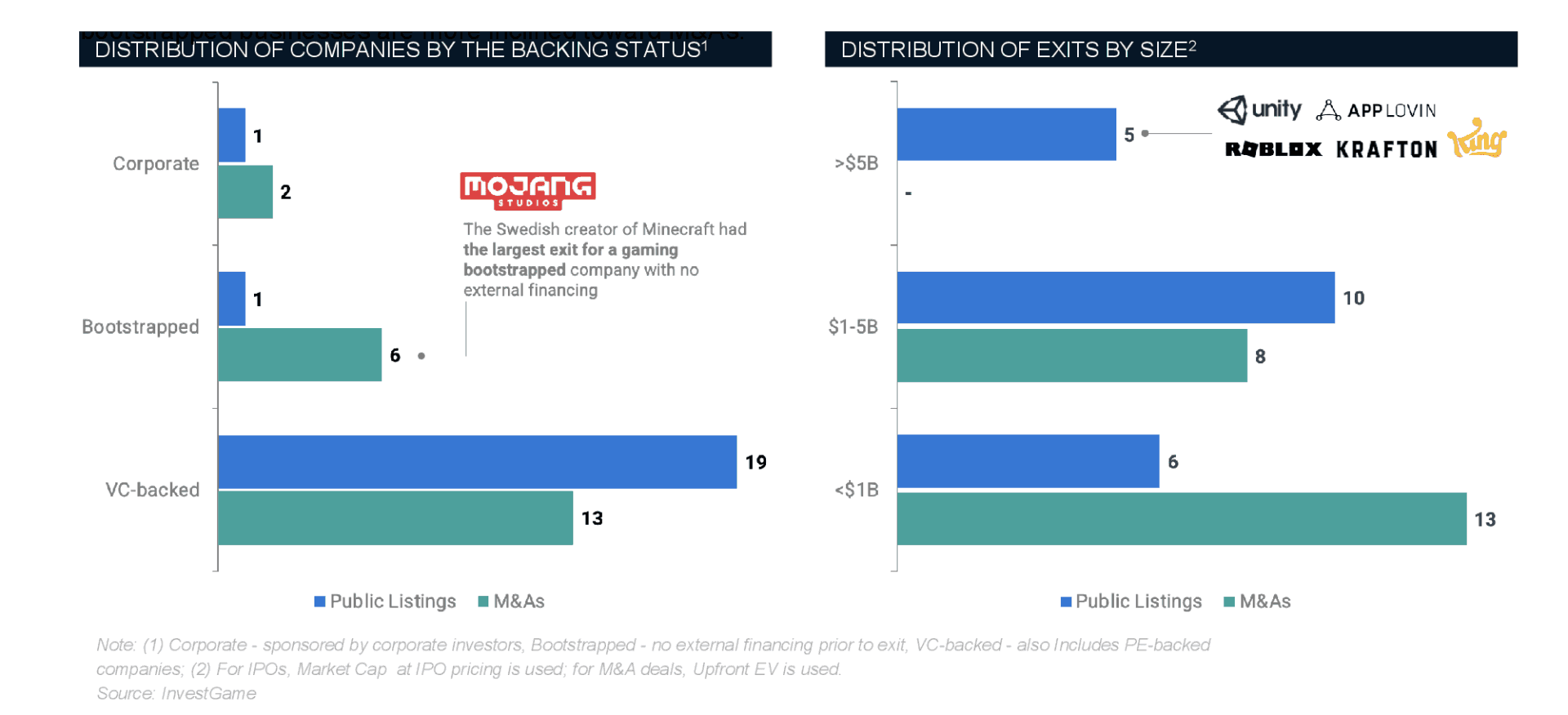

VC-backed companies represent ~75% of all exits, with listing as the preferred route, while bootstrapped businesses lean toward M&A

VC-backed companies dominate the gaming exit scene, making up about 75% of all qualified exits (valuations above $500m). This underscores venture capital’s critical role in helping gaming startups achieve blockbuster outcomes. Notably, around 60% of VC-backed exits were public listings, showing a preference for pursuing a public route rather than selling a controlling stake. Of those VC-backed companies, 18 reached unicorn status (valuations above $1B).

Meanwhile, bootstrapped businesses favor M&A, accounting for six M&A deals and just one IPO. Interestingly, there were five unicorns – Mojang, SpinX Games, Techland, Outfit7, and GDEV. Among them, only GDEV (NASDAQ: GDEV) is publicly listed, while the others took a traditional full sale path. This shows that the right product-market fit can propel studios to billion-dollar heights even without external funding.

Corporate-backed companies (those formed within larger holdings before being spun off) had a more modest impact: one public listing and two M&A deals. These businesses often leverage strategic synergies with their parent entities, but their exit count remains relatively small compared to VC-backed and bootstrapped studios.

Exit size and time to liquidity

As for exit valuations, public listings naturally aim for a higher bar — deals above $5B have so far been exclusive to IPOs—while M&A dominates the sub-$1B category with 13 deals, making it the go-to choice for smaller gaming startups. Public listings work best for companies that have already hit large-scale operations, whereas M&A often delivers quicker liquidity for those at a smaller scale. Another factor is that many publicly listed gaming peers were previously backed by VC/PE investors, which diluted founder ownership. As a result, founders often target higher valuations to secure meaningful returns.

Mobile gaming’s rapid development cycles, broad accessibility, and colossal player base put it front and center for both M&A and public listing exits. This leadership extends to the number of high-value exits and the time it takes to achieve them. On average, it takes around 8 years for a successful mobile gaming studio to exit—about 40% faster than PC & Console studios, which typically need 13 years due to longer development cycles and more challenging marketing and distribution requirements.

A more intriguing angle is how long it takes for VC-backed businesses to hit their first exit—around 9.5 years. This is mainly because they aim for higher valuations through public listings due to heavily diluted cap tables, which would otherwise make exits less rewarding for founders. In contrast, bootstrapped businesses, where founders keep more control and face less external pressure on exit valuations, often see liquidity at around 7 years, though usually at lower valuations (as mentioned earlier).

Considering these, a successful gaming exit takes an average of 7–9 years. This is a lengthy cycle that investors should consider when considering gaming funds’ returns (DPIs) and the natural lifecycle of gaming studios.

Conclusion:

Key findings of our analysis:

- The gaming market has seen 42 successful (above $500m valuation) first-time exits over the last decade, with roughly 75% of those being VC-backed businesses — enough fuel for gaming investors to show decent returns to their LPs and for LPs to maintain trust in these gaming ventures.

- Mobile gaming companies have been favored for exits, accounting for a 75% share overall. This dominance reflects the shorter product lifecycles and quicker time to initial liquidity found in mobile.

- On average, gaming companies take 7–9 years to achieve their first exit, with mobile-focused startups tending to exit 40% faster than PC & Console studios.

- The preferred exit route depends on ownership status. Bootstrapped companies typically lean toward M&A at reasonably lower valuations (usually below $1B), while VC-backed peers often aim for public listings and push for higher valuations (often above $5B).

The last decade shows that gaming isn’t just a “hit-driven” business — it’s a proven avenue for founders and investors seeking solid returns. With 42 successful exits above $500m since 2014, and the majority of them backed by VC funding, the data speaks for itself: mobile titles thrive thanks to shorter development cycles, while PC & Console studios continue to build large-scale franchises that can also catch buyers’ eyes. Mobile’s dominance may face challenges in the coming years as platforms reach maturity, evolving policies (e.g., IDFA) take effect, and competition among mobile studios—already fierce—continues to rise.

Whether you’re bootstrap-focused and leaning toward a quicker M&A exit or aiming for a billion-dollar IPO with significant investor support, you can expect it to take 7–9 years on average to reach that milestone. And while the market’s cooled since the heady days of 2021, there’s still a steady flow of exits each year, suggesting that gaming remains a healthy ecosystem for entrepreneurship and investment. As the industry matures, it may be more challenging for newcomers to recreate the meteoric rise of giants like Roblox or AppLovin, but the market is still full of surprises. If you’ve got the right team, vision, and product-market fit, the doors to meaningful success are far from closed.