NCSOFT’s $202m JustPlay Bet Anchors Its Casual Gaming Expansion

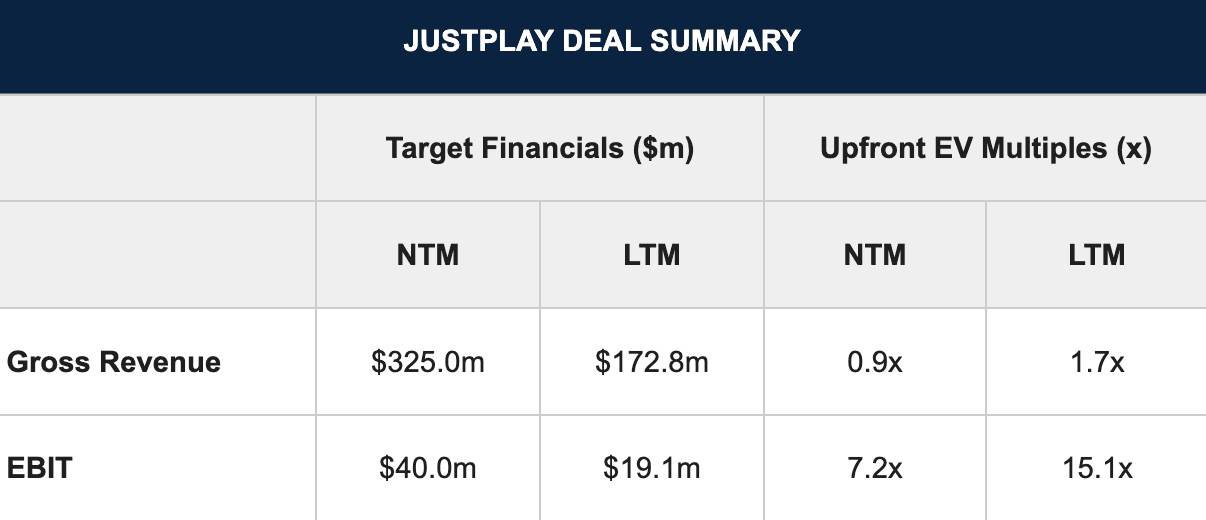

NCSOFT (KRX: 036570), the South Korea-based video games developer and publisher behind the Lineage franchise and Guild Wars 2, is acquiring a 70% stake in Germany-based mobile platform company JustPlay for ~$202m (KRW 301.6B). The remaining 30% equity will be acquired through call and put options with pricing tied to JustPlay’s future operating performance. The deal is expected to close by Apr 30, 2026. JustPlay, founded in 2020 by former AppLovin employees and headquartered in Berlin, provides a reward-based casual gaming platform where users play mobile games (puzzles, card games, arcade titles) and earn real-world rewards via PayPal and gift cards. The company recorded $172.8m in Revenue and ~$19.1m in operating profit (EBIT) in 2025, with ~70% of total revenue generated in the US and Canada, demonstrating a strong presence in Tier-1 markets. Following rapid growth in 2025, JustPlay is projected to generate $65.2m in Revenue and $7.5m in EBIT in Q1’26, with annual results in 2026 expected to reach $325m in Revenue and $40m in EBIT.

JustPlay represents NCSOFT’s largest casual gaming deal to date. At an implied equity value of ~$289m (used as a proxy for enterprise value given the absence of disclosed cash or debt), the deal values JustPlay at 1.7x LTM Revenue and 15.1x LTM EBIT. These multiples align with the recent AdTech peer multiples: for example, Liftoff, which drew General Atlantic investment, traded at comparable levels 15x–16x LTM adj. EBITDA ahead of its IPO filing. However, the Liftoff filing was subsequently withdrawn amid market volatility.

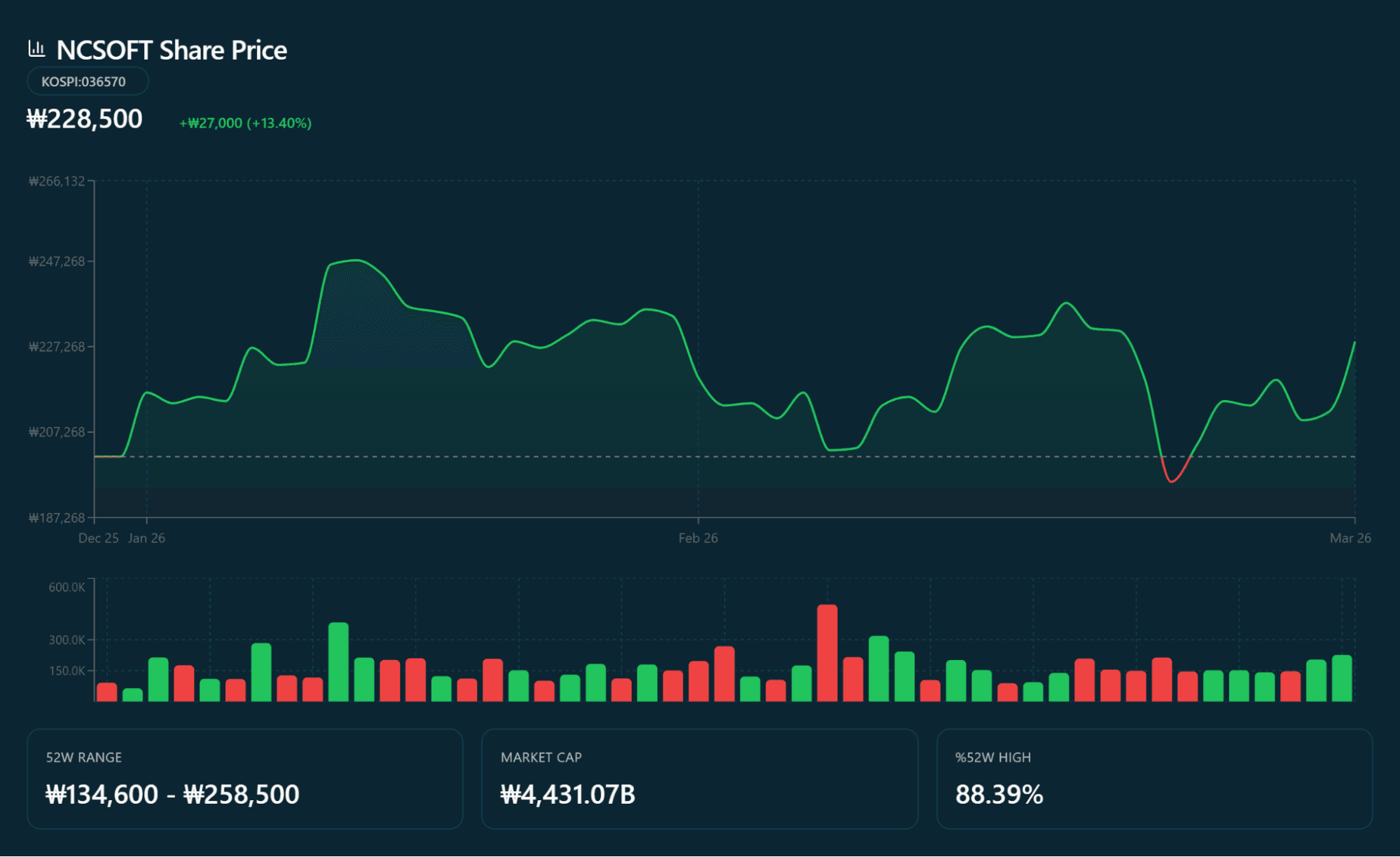

NCSOFT’s stock has demonstrated resilience in early 2026, securing a 13.4% year-to-date gain as of Mar 13, 2026. Following management’s recent announcement of a long-term roadmap, shares recovered to KRW 228,500 (as of Mar 13), which signals broader investor confidence in NCSOFT’s casual gaming pivot.

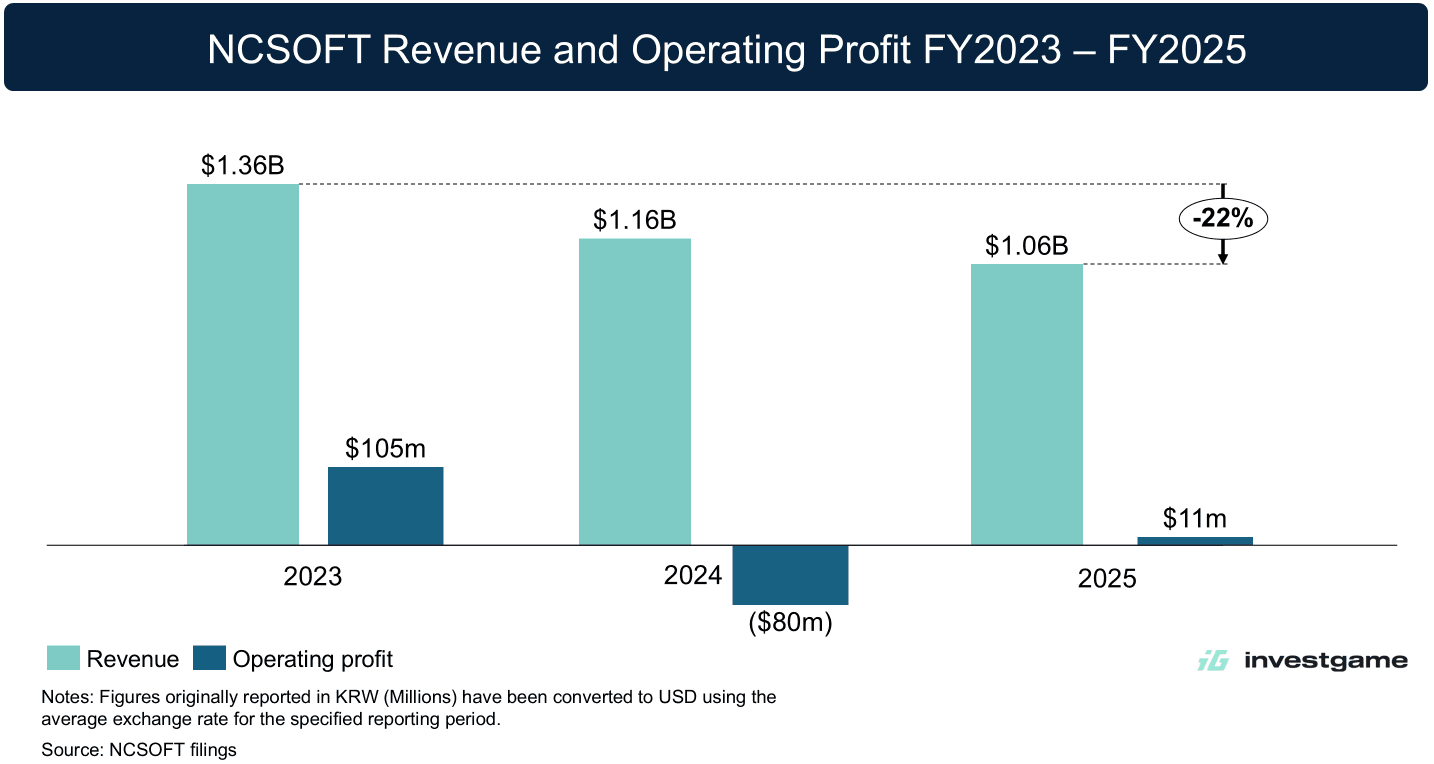

The acquisition comes as NCSOFT navigates a challenging financial period:

- Revenue has fallen 22% over the last two years, placing top-line performance below 2017 levels as the company has transitioned legacy IP to mobile platforms, where rising user acquisition costs and post-COVID player fatigue have compressed margins.

- NCSOFT posted an operating loss in 2024 (its first since its 2000 IPO), driven by a surge in labor costs from a broad organizational restructuring and high marketing expenses for the global PC & Console launch of MMORPG title Throne and Liberty.

- The 2025 turnaround was primarily driven by strict cost discipline rather than organic growth. While reported income was modest, the underlying performance, including one-time severance payments, reached a reported operating income of ~$11m (KRW 16.1B) with only ~1% profitability margin.

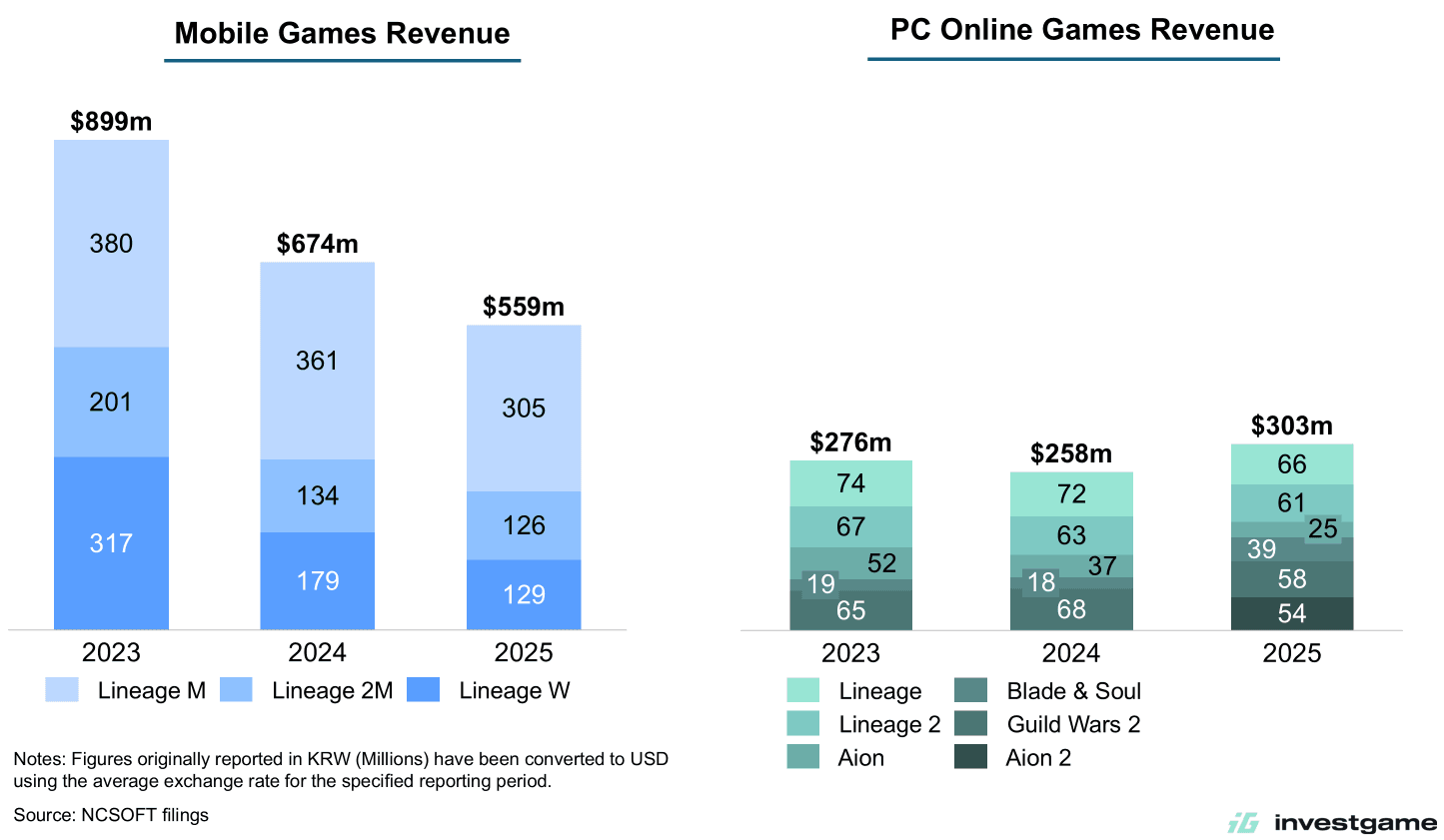

One of the core NCSOFT challenges is the declining mobile revenue of Lineage IP, which has fallen by ~38% over the last two years. This downturn stems primarily from consumer backlash against aggressive “pay-to-win” mechanics and intense competition from “Lineage-like” rivals, including Kakao Games and Wemade. The PC segment showed encouraging growth in 2025, supported by Aion 2 and the Guild Wars 2 expansion, but it was not large enough to offset the mobile erosion.

The new strategy, unveiled at the Mar 12, 2026, management briefing, moves away from a business model centered on a “Lineage-oriented” ecosystem toward the following three core pillars:

- Enhancing legacy IP through refined live-service operations and regional expansion for Lineage, Aion, Guild Wars 2, and Blade & Soul, projected to sustain ~$1.1B (KRW 1.5T) in annual cash flow;

- Securing new IP across shooters, subculture (anime-style), and action RPG genres, with a pipeline of 10+ internally developed and 6+ published titles by 2029;

- Expanding into mobile casual gaming through acquisitions and publishing partnerships. As stated by Co-CEO Park Byung-moo, “the past two years have been dedicated to laying the groundwork for future growth.”

NCSOFT is pivoting away from its hardcore RPG roots by building a new casual gaming ecosystem through recent acquisitions, including a 67% stake in Singapore-based Indygo Group for $103.8m and the purchases of South Korea-based Springcomes and Moving Eye studios. The ~$202m acquisition of JustPlay serves as the anchor for this new ecosystem, shifting the company’s operational model for 2026 by bringing:

- Scaled and rapidly growing reward-based gaming platform with 25 million+ users;

- New traffic acquisition channel at a time when UA costs are rising industry-wide, allowing NCSOFT to cross-promote its own titles (e.g., PUZZUP: AMITOI) at favorable rates;

- Sophisticated AdTech algorithms for player behavior analysis and advertising optimization going forward.

The company aims for $3.5B (KRW 5T) in revenue by 2030 with a 15% return on equity, more than triple its FY’25 revenue. NCSOFT’s ability to integrate its newly acquired studios into a coherent casual ecosystem while simultaneously revitalizing its MMORPG portfolio will determine whether this strategic pivot delivers on its ambitious targets. We will continue to monitor NCSOFT’s integration progress and the performance of its expanding casual portfolio.