This article is based on our Weekly News Digest #15 from 17.04.2023. If you want to receive such analyses first, be sure to subscribe to our weekly newsletter. There, we analyze the largest deals, elaborating on the financials and strategy behind, while also covering the smaller transactions of the week.

Japan-based gaming giant Sega (TYO: 6460) has announced the acquisition of Finland-based mobile gaming company Rovio (HEL: ROVIO) for approximately $783m (€706m), or €9.25 per share and €1.48 per option. The deal is expected to close in Q3’23.

The price comes as a 63.1% premium to the closing price of January 19, 2023 — the exact date Playtika announced its intention to acquire Rovio with a 55% share price premium. Unlike with the Playtika’s bid, Rovio’s board of directors has already agreed to the deal.

Considering Rovio’s Revenue of ~$347m (€317.7m) for the year of 2022, the sum of the acquisition implies 1.7x EV/Revenue and 12.7x EV/EBITDA multiples, which is slightly bigger compared to the multiples from the Playtika’s proposal.

Multiples based on Rovio’s 2022 financial performance.

When it comes to Rovio’s current position on the market, we have already expressed our thoughts on that in one of our previous digests, when Playtika announced its plans to acquire the Finnish company. However, to get the full picture, we will reiterate some of those highlights there.

To us, it seems like Rovio’s valuation before the acquisition talks was significantly underrated. Just before the first bid from Playtika, the pre-proposal enterprise value implied 0.77x EV/Revenue, considering the company’s Revenue of €319.7m for Q4’21-Q3’22. For comparison, looking at the other publicly traded gaming companies, we see the EV/Revenue multiples closer to 1.5x or higher: Stillfront — 1.82x, Playtika — 2.28x (before the proposal). What Playtika (and Sega) did was bring the company’s valuation closer to that of the market, rather than overvaluing the company.

Of course, lower valuations are partially explained by the current state of the public markets, but there is much more to it in case of Rovio. The company went public in 2017 with €11.50 share price, which is almost two times higher than that of the day before Playtika’s proposal. Founded in 2003, Rovio is best known as one of the pioneers of touch-screen gaming, as well as the creator of the legendary Angry Birds franchise. Since 2009, when the first Angry Birds game came out, the company launched 20 more games in the series, as well as several spin-offs and transmedia products.

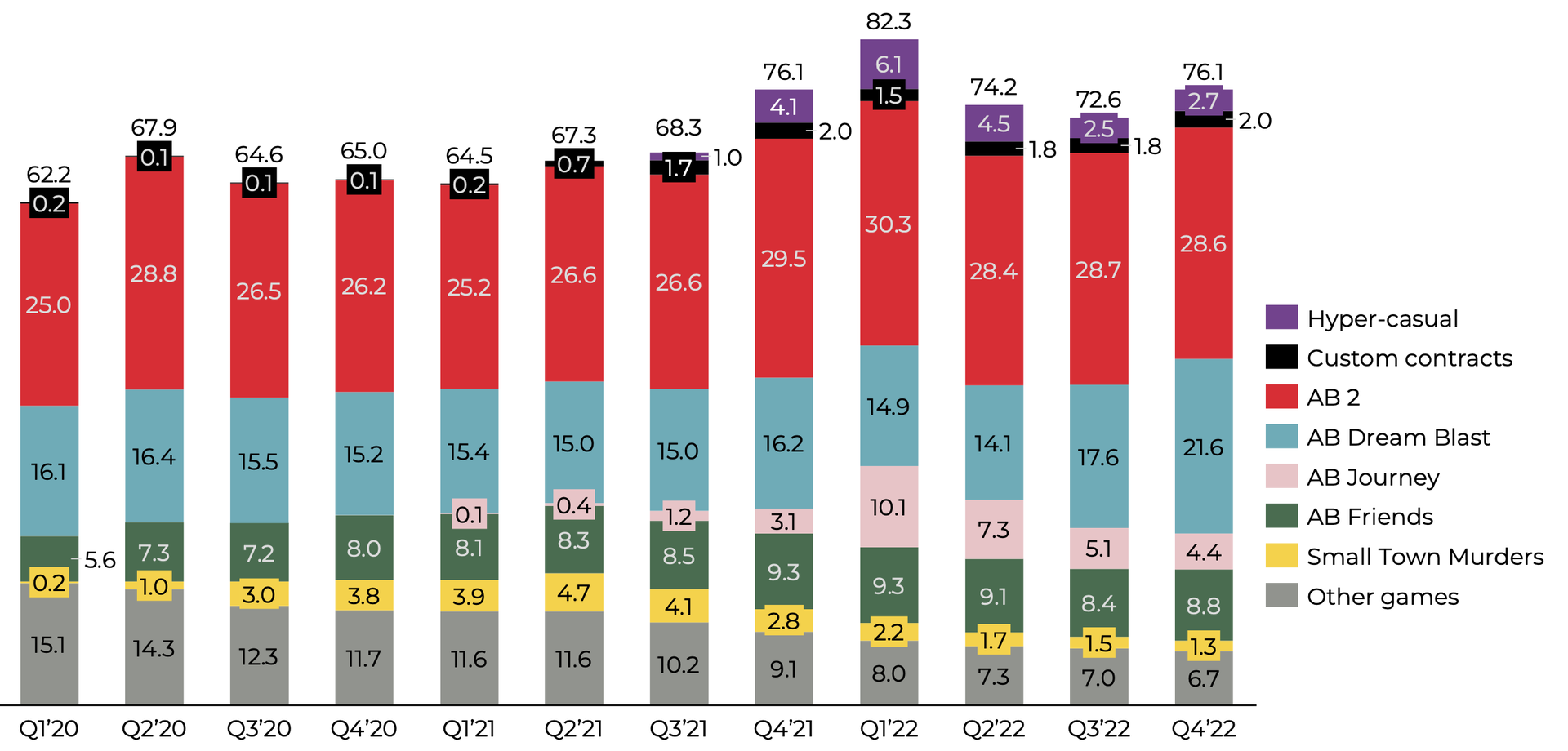

Games gross bookings and custom contracts, €m. Source: Rovio

However, the tremendous legacy is where most of both the strengths and the risks of the company come from. Rovio’s currently best-performing title, Angry Birds 2, was released back in 2015. For comparison, in Q4’22, the latest installment in the franchise, Angry Birds Journey, generated 6.6x times lower Revenue than Angry Birds 2. The second best-performing game, AB Dream Blast, came out in 2019 and is also pretty far behind AB2. That said, Rovio seems to be struggling to reach its past heights with new installments in the series. Nevertheless, despite the dependence on the company’s older games, the company had a solid €182m of cash and cash equivalents on its balance at the end of 2022. These resources not only support the company’s current operational activity, but also may allow it to continue working on the 10 new titles that are currently in development.

So why did Sega decide to go for the acquisition?

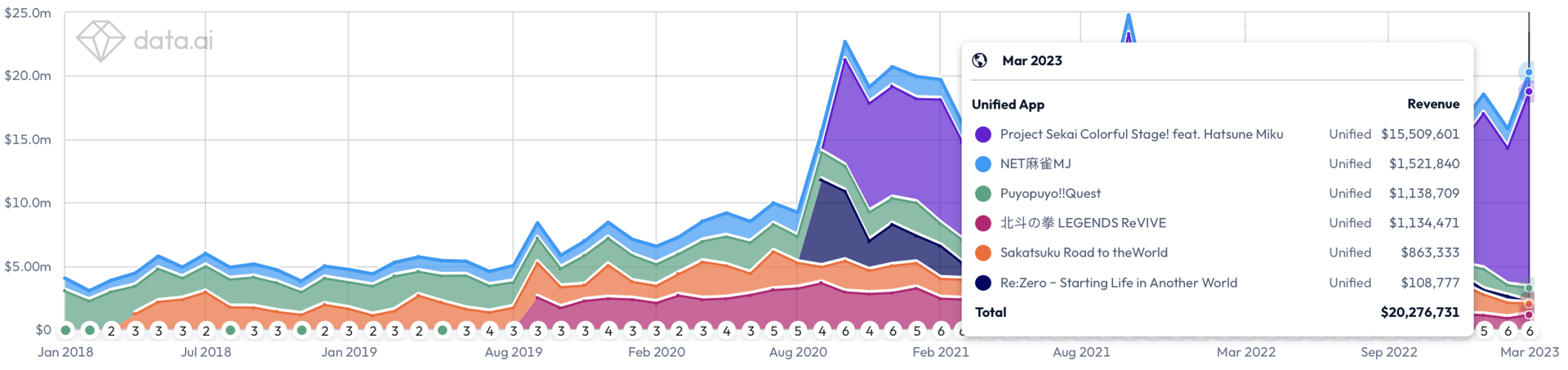

First, it’s about further mobile expansion. Though Sega is best-known for its PC & Console gaming titles, it has a solid mobile gaming portfolio that generated around $264m of IAP Revenues for the last 12 months, according to data.ai. Most of the Revenue is generated by the rhythm game Project Sekai Colorful Stage Feat. Hatsune Miku. The most important thing here for understanding the deal, however, is that the vast majority of mobile Revenue is coming from Japanese players. Acquiring Rovio will allow Sega to geographically diversify its mobile Revenue flows.

Source: data.ai

Apart from the geographical expansion, the acquisition will bring additional expertise across many segments of mobile gaming: while expanding the Angry Birds franchise, Rovio has gathered expertise across various genres — not only casual and puzzles, but blast, side-scrolling shooter, arcade racing, RPG, and even a Roblox game (yet casual is where the company has its greatest expertise). We can also imagine Angry Birds-based special events or other IP collaborations in various mobile games by Sega.

Second, It’s about IP. Yes, we see that new Angry Birds games don’t reach the results of their older installments. However, it is still a well-known and widely recognizable franchise with its own merchandise, comics, film, and TV adaptations. The latter is something Sega has been especially successful in lately — Sonic the Hedgehog movie brought in $319m at the box office, while the sequel generated $405m. The Angry Birds Movie showed similar numbers with $352m box office. Thus, the deal may bring potential crossovers not only in gaming, but in other transmedia activities.

Speaking of crossovers, we have already seen one back in 2015, in Sega’s West-oriented mobile game Sonic Dash. The game had a special event, where gamers could play a set of themed Angry Birds levels with Sonic in them. Considering how many things based on the Sonic franchise we have seen lately, there are more opportunities for crossovers today than ever before.

Why Sega, not Playtika?

It’s still not 100% clear. However, when we were writing about Playtika’s bit, we mentioned Playtika shutting down its subsidiary gaming studio Seriously, laying off 600 employees (more than currently work in Rovio), after laying off 250 people before that. We assumed that this “might be serious reasons for Rovio not to go for the deal, if there happen to be no tangible business and synergy opportunities between the companies.”

We don’t know whether Playtika’s layoff history influenced the decision, but if we are speaking about synergies, there seems to be much more between Sega and Rovio: both have strong international IPs that have had a significant influence on the gaming industry as a whole; both have success stories of transmedia activities, and both have IPs that can appeal to younger and older audiences — in other words, on the surface at least, both companies have a lot to offer to each other in terms of creative and business collaboration.

But let’s also bear in mind that mobile gaming is going through hard times: post-IDFA pressure, increased UA costs, and not-so-efficient app store features, among other things, make it much harder for new titles to survive, much less prosper. Even the above-mentioned Playtika has stopped producing new games until the mobile market environment changes. In this sense, Rovio’s owners may have found a great exit strategy in the Sega deal.

Get the weekly digest on all the latest gaming transactions, with the number and size of the deals, as well as the strategic rationale behind them.