Capital Reset:$19.2B across 362 Swedish gaming transactions (2014–2025); public-market-driven consolidation accelerated during the zero-interest-rate period (2020–2022) and shifted in 2023–2025 toward balance-sheet repair, restructurings, and asset divestments as macro conditions tightened.

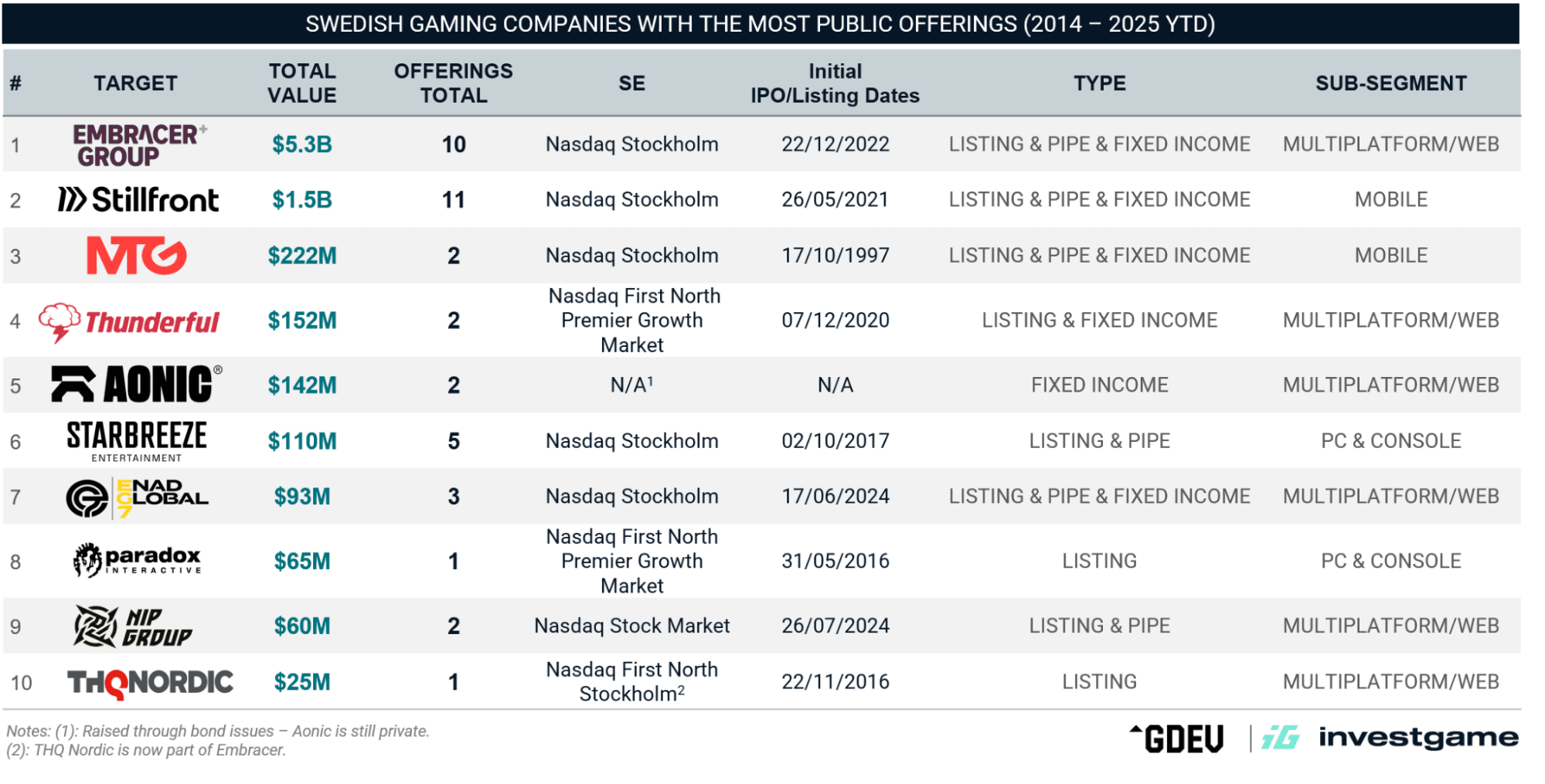

Public Markets Model:Nasdaq First North functioned as a growth-capital venue, enabling early listings for companies such as Embracer, Paradox, Stillfront, and EG7, and supporting roll-up strategies until rising rates and valuation compression undermined the multiple-arbitrage model.

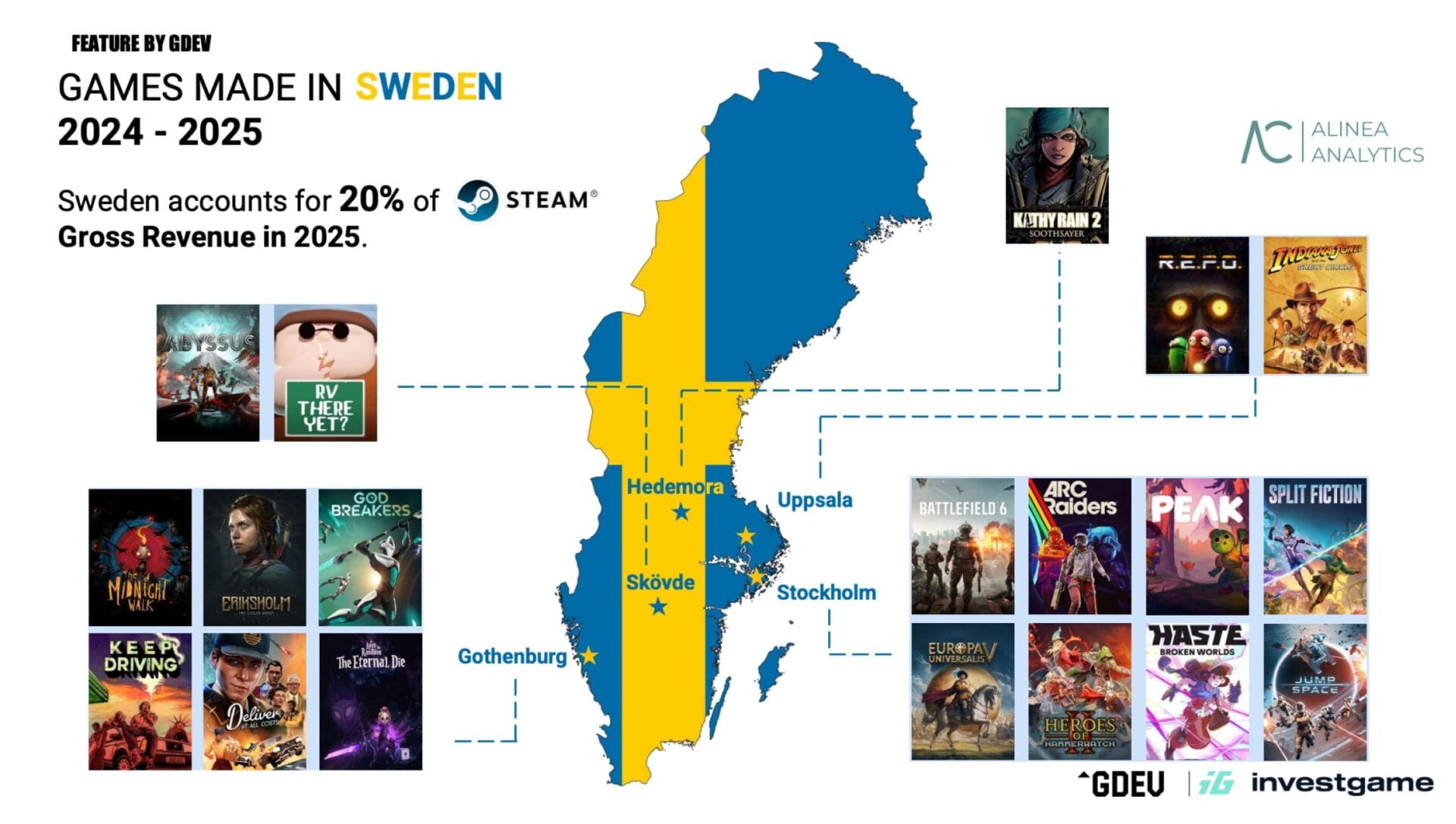

Creative Output: Sweden accounted for ~20% of Steam’s 2025 gross revenue and continued shipping global PC, console, and mobile hits during 2023–2025, even as public gaming groups underwent restructurings and balance-sheet repair.

Sweden accounts for roughly 20% of Steam’s 2025 gross revenue and, in the 2024–2025 release window, Swedish developers delivered five of Steam’s global top-10 bestsellers (Battlefield 6, R.E.P.O., Peak, ARC Raiders, and Split Fiction), according to Alinea Analytics. Where larger markets scale through volume — more studios, more capital, more releases — Sweden generates outsized returns per studio and is the world’s second-largest producer of unicorns per capita.

You can call it “hit density”: the ratio of global breakouts to ecosystem size. Sweden has never dominated gaming VC headlines the way the US, UK, or Turkey do, yet its creative output per dollar deployed is unmatched. More than 1,100 game companies cluster around Stockholm, Malmö, and Gothenburg, producing AAA franchises (Battlefield, Indiana Jones, the Paradox catalog), survival dominance (Valheim, V Rising), viral indie breakouts (R.E.P.O, RV There Yet?), and Helldivers II — Sony’s fastest-selling first-party title to date.

Sweden’s strength spans both sides of the gaming industry. In PC & Console, studios like Arrowhead, Embark Studios, Paradox (STO: PDX), MachineGames, and Coffee Stain Group (STO: COFFEE b) built global franchises through design excellence and engineering depth. In mobile, King’s $5.9B exit to Activision Blizzard validated Swedish operators at scale — and opened the door for holdings like Stillfront (STO: SF), MTG (STO: MTG), and Embracer (STO: EMBRAC B) to build substantial mobile portfolios through public-market-funded M&A. These consolidators became Europe’s most aggressive acquirers during the era of zero interest rates.

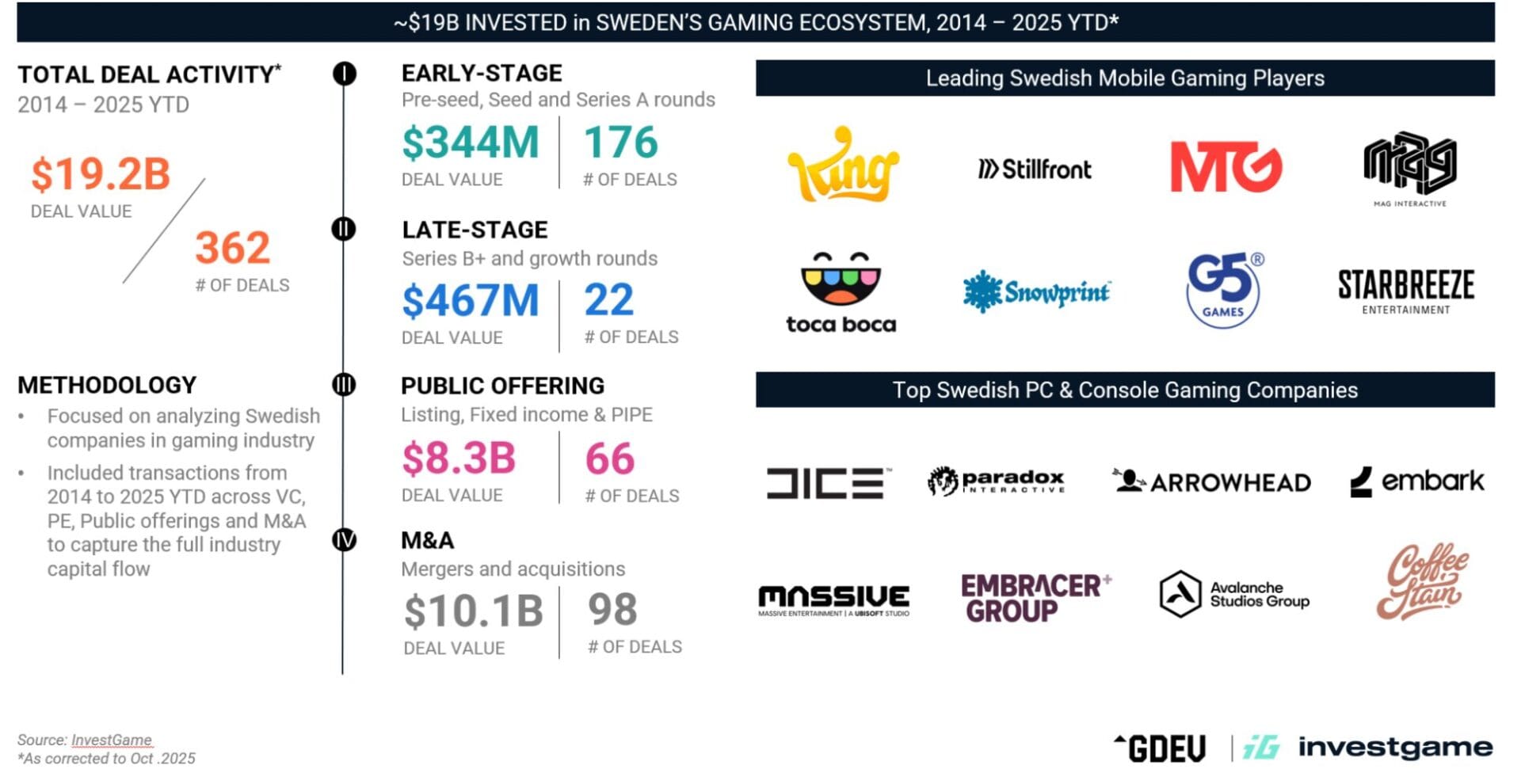

Between 2014 and 2025, Sweden recorded $19.2B in gaming transactions across 362 deals — spanning investments ($811m across 198 deals), public offerings ($8.3B), and M&A ($10.1B). The public-market era powered unprecedented consolidation. When interest rates rose, organic growth slowed down, valuations collapsed, and the capital machine reset. Several of Sweden’s most active public acquirers underwent strategic reviews, restructurings, and balance-sheet repair — a sharp contrast to the aggressive M&A pace that defined the sector just four years ago. However, the creative engine — the studios shipping hits across PC, console, and mobile — kept running.

This Feature examines how Sweden’s capital model rose, why it reset, and what the continued hit production reveals about where gaming value actually compounds.

For a detailed analysis, check out the accompanying report:

Methodology: Analysis covers Jan’14 – Oct’25, including M&A, public offerings, debt/fixed-income, and VC/PE rounds where the target/issuer is headquartered in Sweden. Deal values reflect disclosed upfront consideration plus announced earn-outs. Excludes internal restructurings and undisclosed transactions.

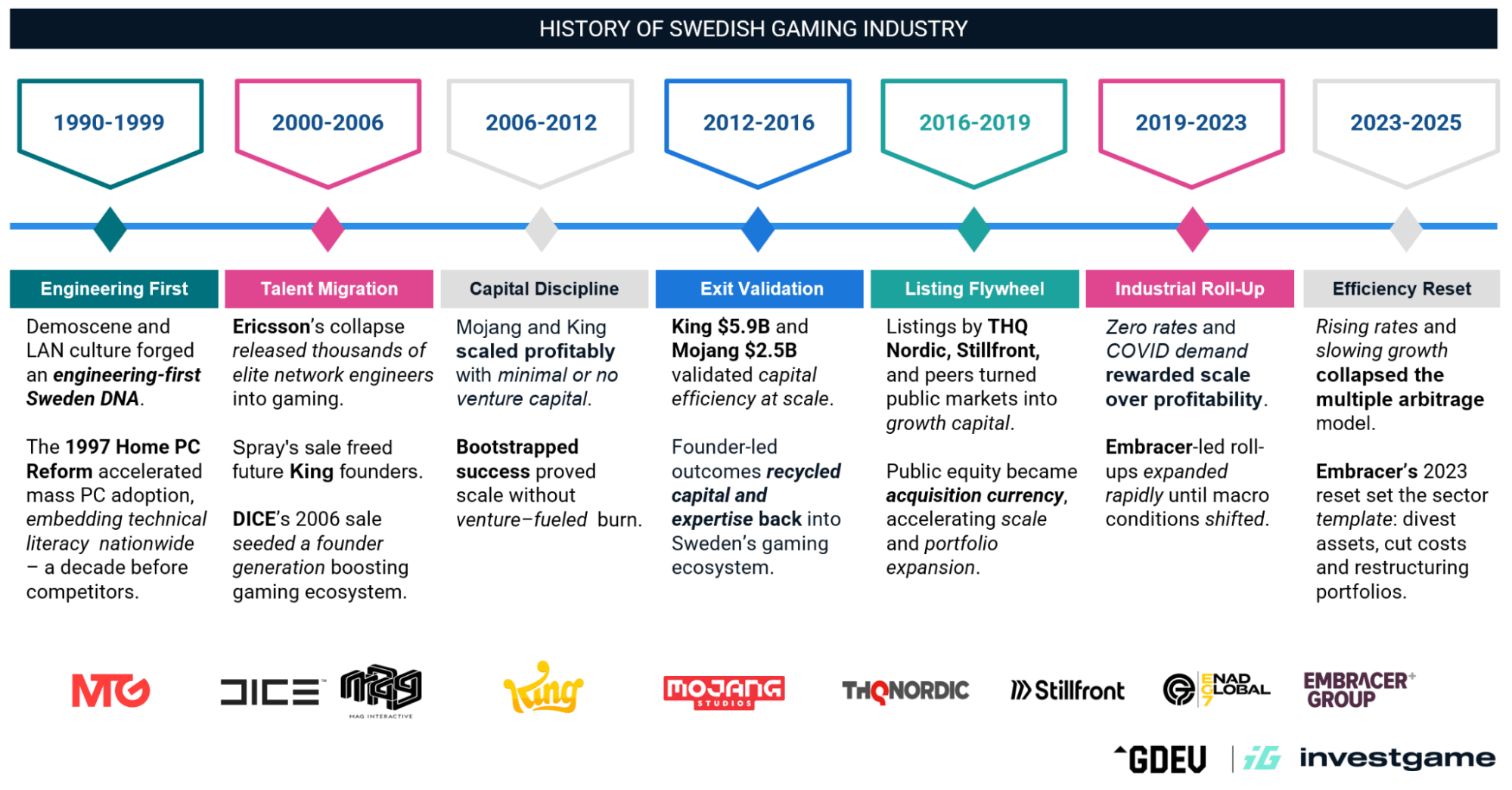

The Foundation (1990–2006): Engineering Before Finance

Sweden’s gaming dominance emerged from a “Triple-Helix” that no other European market replicated: state policy, corporate collapse, and underground subculture.

In the 1990s, Sweden’s “Demoscene”—groups like Fairlight competing to produce real-time audiovisual experiences — cultivated an engineering culture built on first principles. Unlike the US, where tech emerged from academic or military institutions, Swedish tech was born from creative coding subcultures. The 1997 Home PC Reform supercharged this energy. By allowing employees to lease computers via pre-tax salary deductions, the government achieved 70% household PC penetration by 2001, years ahead of most European markets.

The transition from hobbyist to professional was catalyzed by an unexpected source: the collapse of Ericsson. Between 2001 and 2003, Ericsson cut its Swedish workforce — specialists in latency, connectivity, and server-side stability. When gaming moved from offline to always-online, Sweden already had the network engineers to build it. MAG Interactive’s founders met at an Ericsson research lab; King’s founders met at Spray, a dot-com portal that collapsed in 2000.

By 2006, Electronic Arts acquired DICE for ~$93m — buying not just a leading gaming studio, but the engineering capability that later produced the Frostbite engine (released in 2008), which went on to become central to EA’s technology strategy. The acquisition validated that Swedish “tools” were as valuable as Swedish “content.” It also explains why DICE veterans have spawned an entire generation of studios: Embark Studios (founded by Patrick Söderlund, former EA Chief Design Officer), Sharkmob, Neon Giant, TTK Games, and Liquid Swords all carry the “DICE Mafia” DNA of high-fidelity technical engineering.

The Exit Decade (2006–2016): Capital Efficiency as Competitive Advantage

The following decade proved that Swedish studios could achieve billion-dollar outcomes through extreme capital discipline rather than venture-fueled burn.

Mojang remains the purest expression of the model. Founded in 2009, the studio never raised venture capital. Minecraft was bootstrapped and profitable from day one. Before founding Mojang, Minecraft creator Markus “Notch” Persson worked as a developer at King. Microsoft’s $2.5B acquisition in 2014 flowed directly to founders — not institutional investors.

King followed a more complex but equally disciplined path. After narrowly avoiding bankruptcy in 2003, the studio became a cash-flow fortress. When King raised $43m from Apax Partners and Index Ventures in 2005, it wasn’t to survive — it was to scale. In fact, the majority of that round was for early liquidity. By the time Activision Blizzard acquired King for $5.9B in 2016, the studio had been cash-flow positive for over a decade.

This “Engineering-over-Finance” mindset proved that in Stockholm, venture capital was a strategic tool, not a life-support system. These exits rewired local expectations. They legitimized gaming as an institutional asset class in Stockholm. More importantly, the capital stayed in the ecosystem — founders became angels, executives became operators at the next generation of studios, and the “King Mafia” spread mobile expertise across the market.

Two structural factors amplified this efficiency. First, the “Small Market Paradox”: Sweden’s 10 million population is too small to sustain locally oriented industrial leaders, forcing companies to build for global audiences from day one — a pattern seen not only in games, but also in Swedish breakout exports like Spotify, H&M, and even the Eurovision song contest. Second, Sweden’s social safety net lowers the personal cost of failure. Many Swedish hits — Minecraft, Valheim, R.E.P.O. — started as passion projects. The safety net allowed developers to spend 12–24 months pre-revenue, prioritizing technical ambition over early monetization. Born-global thinking plus low-consequence failure: Swedish founders attempt technically ambitious projects that peers elsewhere might never start.

The Growth Listing Era (2016–2019): Public Markets as Venture Capital

The most distinctive feature of the Swedish model is the Stockholm Stock Exchange (Nasdaq First North). Unlike US markets, where IPOs function as “end-game” liquidity events, Sweden uses public listings as growth capital tools. Small gaming studios could list on First North far earlier than they could in London or New York, providing “exit-lite” liquidity that kept founders engaged while unlocking capital for expansion.

Between 2016 and 2019, a wave of now-iconic companies entered public markets:

THQ Nordic (later Embracer) listed in 2016 at a $210m valuation, providing the initial currency for what would become the world’s most aggressive roll-up machine.

Paradox Interactive, listed in 2016, bringing a premium PC strategy publisher into public markets and later using that platform to scale a long-tail, DLC-driven model.

Stillfront, listed in 2015, perfected the mobile strategy playbook, evolving from niche publisher to global holding entity.

Toadman Interactive (later EG7) was listed to fund its transformation from a work-for-hire studio to a global publisher.

G5 Entertainment shifted to 100% F2P and moved to the Stockholm Main Market as Hidden City became a global top-earner.

The model created a flywheel: public markets provided capital, capital fueled acquisitions, acquisitions expanded IP portfolios, and increased scale boosted stock prices. By 2019, Swedish gaming had developed a unique capital formation infrastructure that would prove both powerful and dangerous in the years ahead.

The Aggregation Era (2020–2022): The Roll-Up Machine at Scale

During the zero-interest-rate period, Swedish holding companies industrialized the roll-up strategy. COVID-era demand and global liquidity created convergent conditions: engagement spiked, capital was cheap, and public gaming stocks rewarded growth over profitability.

The “Multiple Arbitrage” thesis was straightforward. Public groups trading at 15–20x EBITDA acquired private studios at 6–8x EBITDA, funded by highly valued equity and cheap debt. The moment an acquisition closed, the target’s earnings were re-valued at the acquirer’s higher multiple—creating instant shareholder value.

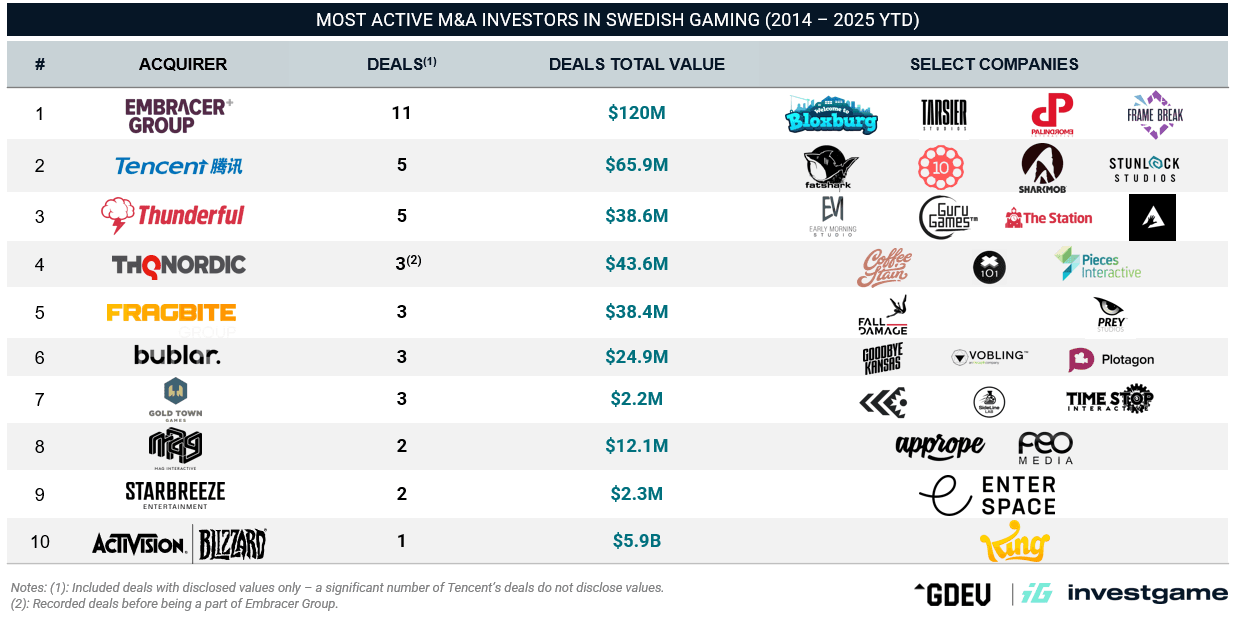

Embracer and Stillfront became the twin engines of Swedish M&A. Embracer acquired Saber Interactive (2020), Gearbox (2021), and Asmodee (2022) as a diversification play, and acquired Crystal Dynamics, Eidos-Montréal, and Square Enix Montréal (2022). By year-end 2022, Embracer had amassed 130+ internal studios and 15,000 employees. Stillfront targeted long-lifecycle mobile cash flow: Storm8 (2020), Jawaker (2021), 6waves (2022). EG7 and Maximum followed the “cluster” strategy, while MTG divested ESL Gaming to Saudi Arabia’s Savvy Gaming Group for $1.05B in 2022, recycling esports capital into mobile gaming.

By the end of 2022, Swedish holding companies controlled a significant share of the world’s middle-market and AA development capacity. The model worked — until macro conditions changed.

The Reset (2023–2025): Efficiency Over Expansion

The macro pivot broke the aggregation thesis. Rising rates increased debt costs. Post-pandemic normalization softened growth. Investors stopped paying for portfolio stories and started underwriting cash flow. While IDFA changes hit mobile gaming broadly, the impact in Sweden was likely smaller given its more PC & Console-weighted ecosystem, and even its flagship mobile success (King) relied earlier on brand-driven marketing rather than pure performance UA.

The Swedish reset had a few catalysts, one of which was the collapse of Embracer’s $2B strategic partnership in May’23. The response became the sector template: reduce leverage, cut CAPEX, sell assets.

Since then, Embracer divested multiple assets, including such big studios as Easybrain, Saber Interactive, Gearbox, and completed operation restructuring. Through these divestments, ~3,000 employees moved out of the group with the sold entities, in addition to ~1,400 direct headcount reductions (8%+ workforce cut). The divestments and restructuring also reduced Embracer’s development pipeline, with projects in production declining from 221 to 141 (approximately 80 fewer titles). With the final accord being the split of business into the three separate, listed independent entities: Asmodee Group (STO: ASMDEE-B), Coffee Stain Group, and Fellowship Entertainment.

Stillfront reorganized into three business areas targeting 200–250 MSEK in annual savings, shifting from M&A growth to margin protection. As of Oct’25, Stillfront is shortlisted to close or divest 10 games by the end of 2025.

EG7 shuttered its original Toadman unit to focus on higher-margin live-service assets like EverQuest.

Thunderful marked the cycle’s clearing price: Atariacquired 82% for $5.2m — effectively pricing equity near zero.

MTG is pursuing a different playbook entirely: exploring a $450m IPO of its Indian subsidiary PlaySimple on the Mumbai exchange, potentially in H1’26.

The 2023–2025 era marked the end of ‘Empire Building’ via financial engineering. The collapse of the Embracer/Savvy deal forced a market-wide pivot to Balance Sheet Repair. From the three-way split of Embracer to Thunderful’s distressed sale to Atari, the narrative shifted from ‘How many studios do you own?’ to ‘How much free cash flow can you protect?’ By 2025, the Swedish market had matured, with survivors like MTG seeking liquidity in global markets (Mumbai) and others like Coffee Stain returning to their roots as specialized, independent-minded operators. The public-offerings market told the same story. PIPE offerings collapsed from $1.8B (2021) to near-zero (2023).

Private Capital: Concentrated and Strategic

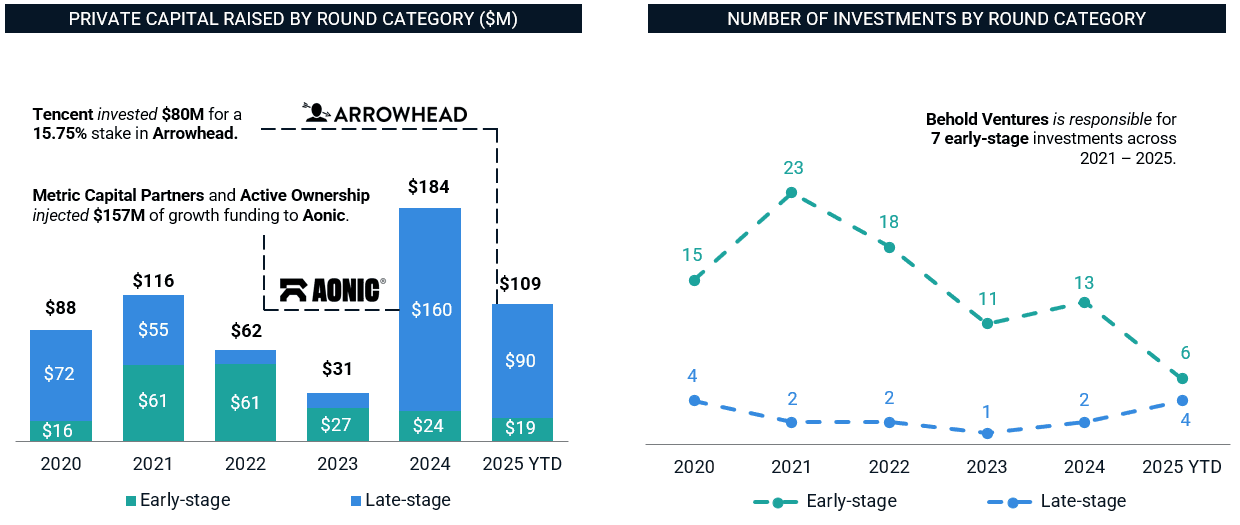

Sweden never dominated gaming VC headlines. Between 2014 and 2025, the ecosystem attracted $811m across 198 private investment rounds — $344m in early-stage (176 deals) and $467m in late-stage and growth (22 deals). Relative to the US, UK, or even Turkey’s mobile-focused VC boom, these are modest figures. But they are consistent with an ecosystem that scaled through public markets and disciplined operators rather than venture-fueled acceleration.

After a deep pullback in 2022–23, private capital returned in 2024 — but the pattern shifted. Late-stage rounds now dominate capital flows, concentrated around a handful of proven operators rather than broad early-stage deployment. Tencent invested $80m for a 15.75% stake in Arrowhead, implying a valuation above $500m for the studio behind Helldivers II. Metric Capital Partners and Active Ownershipinjected $157m of growth funding into Aonic. Early-stage deal count, meanwhile, dropped from 23 rounds in 2021 to 13 in 2024 and 6 in 2025 YTD — a normalization after the peak rather than a collapse.

Swedish studios have long favored capital efficiency over venture-funded growth. Many operate profitably for years before their breakout moments—bootstrapped or sustained by small outside investments—then attract strategic backing after demonstrating execution. The pattern repeats across the ecosystem’s most successful operators.

Embark Studios, founded by former DICE executives including Patrick Söderlund, secured a strategic partnership with Nexon from the outset. Nexon invested $41m at formation in 2018, increased its investment to $137m for majority control in 2019, and completed a full acquisition by 2021 — bringing cumulative investment reportedly close to $300m. The studio released The Finals (2023) and ARC Raiders (2025), both developed with fewer than 100 employees at peak.

Stunlock Studios, the developer of the survival hit V Rising (4M+ copies), secured majority backing from Tencent in 2021. Fatshark, developer of the Warhammer: Vermintide and Darktide franchises, sold 36% to Tencent in 2019 for $56m, with Tencent later increasing to a majority stake in 2021. Paradox Interactive has counted Tencent as a strategic shareholder since its 2016 listing.

The preference for corporate strategic partners over traditional venture capital reflects Swedish studios’ priorities: creative independence, long development timelines, and operational support from investors who understand games as services. These partnerships provide resources without the governance pressure and exit timelines that venture backing typically demands. Private capital isn’t replacing Sweden’s public-market engine—it’s selectively backing operators whose hit density was built on design discipline rather than financial engineering.

Conclusion: The Engine That Keeps Running

The apparent paradox we opened with — 20% of Steam’s gross revenue from an ecosystem simultaneously undergoing balance-sheet repair — now resolves into clarity.

Sweden built two distinct engines over three decades. The first was a public-market aggregation machine: holding companies using listed equity to roll up mobile portfolios and middle-market studios during the zero-rate era. This was a capital-structure play as much as a creative one‚ multiple arbitrage, cheap debt, and scale for scale’s sake. When macro conditions changed, this engine stalled. Balance sheets required repair. Acquisitions stopped. Empire-building gave way to portfolio optimization.

The second engine was the creative core: studios like Arrowhead, Paradox, MachineGames, Coffee Stain, and Embark that built global franchises through engineering depth and design discipline. These operators were often bootstrapped, strategically backed, or stubbornly independent. They never depended on the aggregation machine. They kept shipping hits — Helldivers II, Indiana Jones, Valheim, The Finals, V Rising — regardless of what was happening to holding company stock prices.

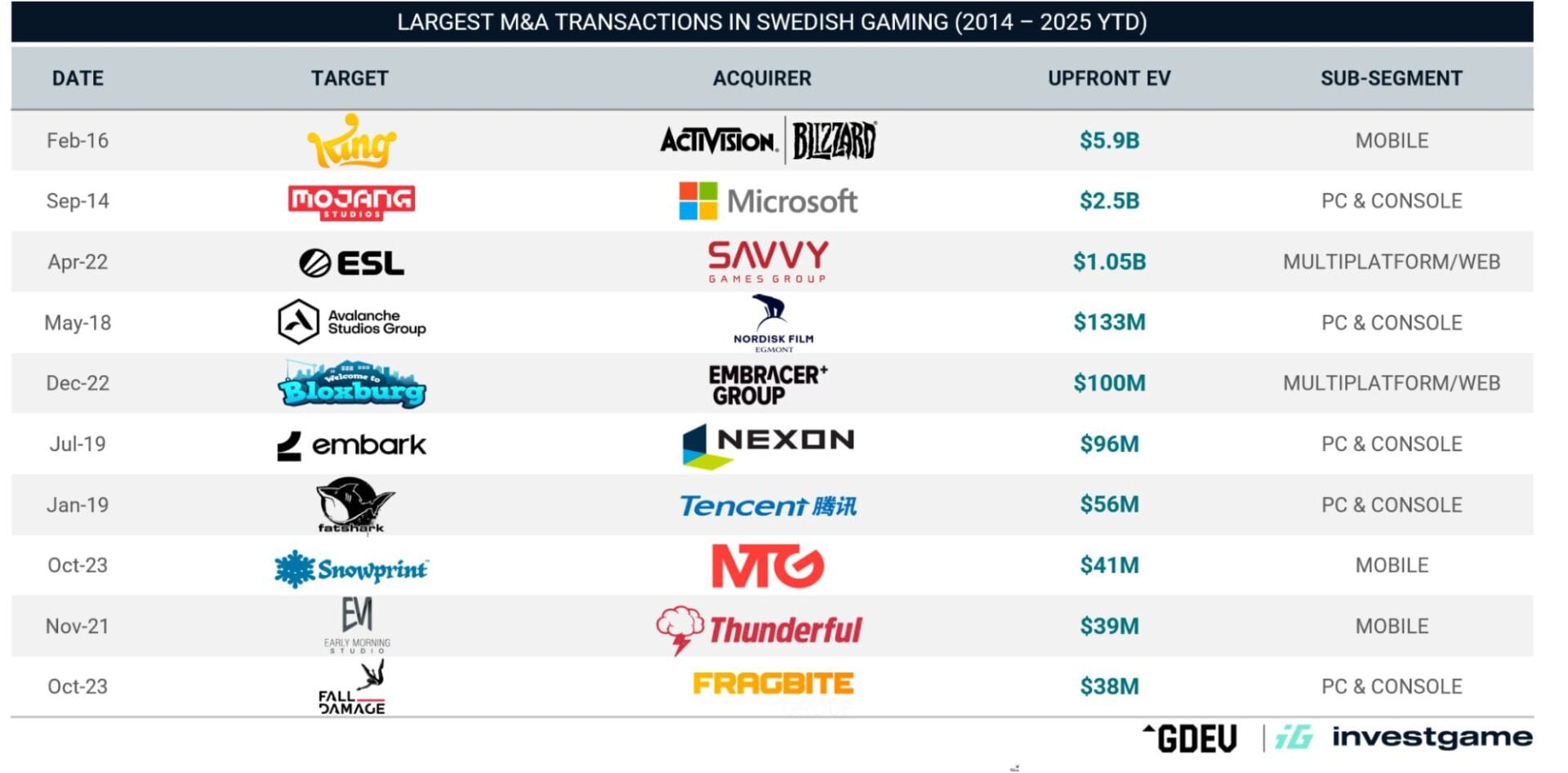

Three landmark exits — King ($5.9B), Mojang ($2.5B), and ESL ($1.05B) — account for 93% of Swedish gaming M&A value, all closing by 2022. Sweden hasn’t minted a billion-dollar exit since. But the track record speaks for itself: strategic acquirers who bet on Swedish talent have been rewarded handsomely. Microsoft’s Mojang purchase delivered a platform-defining franchise; Activision Blizzard’s King acquisition secured mobile’s most durable cash-flow engine; EA’s DICE investment yielded decades of Battlefield dominance – including Battlefield 6, the best-selling game of 2025; and Nexon’s full acquisition of Embark produced back-to-back hits in The Finals and ARC Raiders (Best Multiplayer at The Game Awards 2025). The pedigree is proven. Now a new generation is forming: Tencent’s $80m investment in Arrowhead at a $530m+ valuation, plus a wave of independent studios shipping viral indie breakouts and survival hits, suggest the next chapter of Swedish M&A will be written by strategic buyers who recognize that betting on Swedish execution continues to pay off.

The lesson is not that Sweden’s capital model failed. The public-market era succeeded within its window, creating liquidity for founders and powering Europe’s most aggressive consolidation phase. The lesson is that capital structures rise and fall while creative ecosystems compound. Hit density — the metric that distinguishes Sweden from larger, better-funded markets — was never a function of financial engineering. It was a function of thirty years of accumulated talent, engineering culture, and born-global ambition.

The reset clarified what Sweden’s gaming ecosystem actually is: not a venture market, not a roll-up machine, but a talent cluster that compounds through engineering culture and design discipline. Capital models will continue to evolve. The creative core has proven more durable than any of them.

Thirty years after basement LAN parties helped shape DICE and Sweden’s PC-first DNA, the country remains Europe’s most resilient gaming cluster. The capital machine is resetting.

Huge thanks to our dear friend Phillip Black — an expert game economist and a regular on the DoF podcast — for the extra guidance and thoughtful feedback on this feature!

Subscribe for our weekly newsletter

Get the weekly digest on all the latest gaming transactions, with the number and size of the deals, as well as the strategic rationale behind them.